"smart grid"

State of the Smart Grid Business in 2013

Smart Grid sales across the world in the last 3 years at installed prices have grown by CAGR of approx. 35% and climbed to $36.5 billion in 2012. Given the general global economic demise during this period these figures are remarkable. However they include a steady flow of refurbishment business that has for more than 10 years incrementally improved and smartened up the control and reliability of the electrical network.

If we strip out these numbers then growth in pure Smart Grid is significantly lower. The main task in delivering a Smart Grid has to be in installing and bringing together Smart Grid systems such as AMI, Automatic Distributed Response and Interfacing at the customer end with Distributed Energy and Smart Buildings. This is in order to win “Negawatts” and achieve the main aim of Smart Grid; which is to accommodate the maximum amount of renewable power on the grid and reduce CO2 emissions.

With the exception of smart meters, Smart Grid is only in its infancy in these business areas and as our report http://memoori.com/portfolio/the-smart-grid-business-2012-to-2017/ shows there is still much serious work to be done and roadblocks to be cleared.

The Technology is in Place and the Supply Industry can Deliver

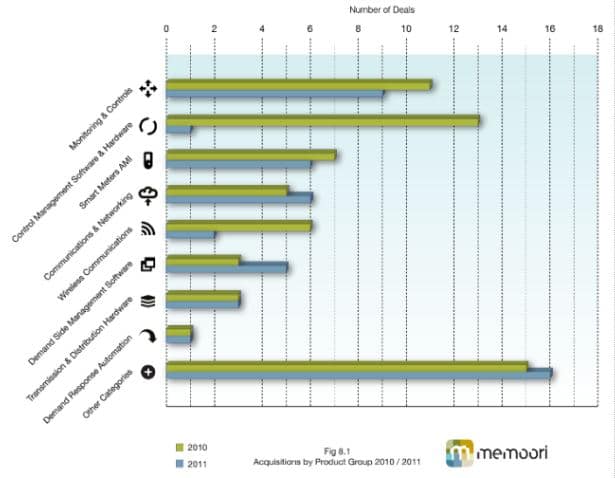

Our report shows that the supply side is changing to meet this challenge. In 2012 $19.5 billion was spent on acquiring and consolidating the Smart Grid supply business almost double the spend in 2011. Investment through Venture Capital amounted to $779 million after adjusting for senior debt finance transactions and although this was a decline on 2011 it fell short of the general decline in the cleantech industry.

The structure is changing with a perceptible but slow move away from the dominance of the international ‘majors’ to the medium and smaller specialist companies who are increasing their share of the business. In addition a significant number of new entrants from outside the industry; from the IT & Comms business, are increasing competition and strengthening the industry. The industry is still too fragmented with hundreds of companies below minimum economic size and consolidation will continue at the current pace for many years to come.

We are confident that the supply side will not hold back Smart Grid’s development. The supply structure is taking on a new shape as the traditional electrical transmission and distribution suppliers are competing with, or forming alliances with, the “new boys” from the digital world of IT, Communications and Controls.

The traditional players certainly have a major role to play, although not a dominant one across all fields of pure Smart Grid. They have the financial muscle to take on major contracts that will become larger with time. The Smart Grid supply industry is in good shape and will not hold back the enormous potential of the new Smart Grid.

The technology is in place to meet the challenge of Smart Grid and there are no known roadblocks here that will restrict its development. ‚Â The new technology surrounding communications and “Big Data” has yet to be proven in the Smart Grid environment however it is already being used in other industries at the required scale.

Regional Country Variations

China & Asia

Asia has still yet to install much of its electrical grid and this creates a double edged sword with the benefit of starting with a pure Smart Grid system not hampered by the problems of a hybrid development but the disadvantage of requiring much larger sums of investment.

On balance it has a stronger potential to rapidly reach large-scale implementation than the other 2 major regions Europe and North America; because it is one part of a major infrastructure plan to provide, energy, transport and communications services for the majority of countries in the region. ‚Â It has strong economic growth that at the moment is less likely to be blown off course. Vast differences exist between the capacity and capability of telecommunications networks in rural and metropolitan areas to play their part and Smart Grid deployment varies enormously across the region.

The countries that lead on Smart Grid development in Asia include Australia, Japan, Thailand, Singapore, South Korea and China. China’s State Grid Corporation has started what will be the largest Smart Grid roll out program with roughly 350 million smart meters to be installed by 2020.

Our report shows that in 2012 China spent more on Smart Grid than any other country overtaking the USA for the first time. They are installing for the most part locally manufactured equipment from indigenous suppliers, but gradually western technology acquired through alliance / partnering agreements is coming through.

North America

Our figures show that up to 2011 North America was the number 1 investor in Smart Grid systems but has now been overtaken by China. This is disappointing given that the 2009 American Recovery and Reinvestment Act provided a major incentive for the industry with more than $4 billion in grant funding for Smart Grid program demonstrations. It does have the strongest supply industry and has spawned a number of impressive startup companies. It is likely to produce the strongest suppliers for the Smart Grid “Big Data” sector that will capture much of the business in the rest of the world. However implementing the demand model could become more of a challenge in the USA than most other developed markets and if so this would drastically hold back Smart Grid growth.

Europe

Europe has some of the world’s most favourable policies for driving Smart Grid deployment. The European Union (EU) has implemented policies on increasing energy efficiency, installing more renewable energy sources, and reducing greenhouse gas emissions all by at least 20% by 2020.

Currently it has some major economic restructuring ahead to solve sovereign debt which is likely to delay these targets and in turn Smart Grid deployment.

The electrical transmission and distribution industry consists of both public and private ownership and is large scale and financially relatively strong. The supply side is strong as European manufacturers are leaders in electrical grid technology and the deployment of Smart Grid. ‚Â On the negative side regulatory policy on standards and interoperability is weak and the decentralised nature of utility markets leads to difficulties in sharing of technology demonstration programs.

The Framework on which to Build Smart Grid is not yet in Place

2 fundamental changes need to be made here if Smart Grid is to deliver. The first is to change the model from its present central structure to a hybrid decentralised one that will allow all the stakeholders to contribute and benefit from. Micro-generation and Micro-grids need to be incorporated into the electrical supply system because they can generate from Variable Renewable Energy (VRE), help balance out supply and demand, deliver locally and make the system more flexible, reliable and efficient.

The second is that it can’t be left to the present owners of the electrical network. Even if this could be organised through the electrical utilities and they could acquire the skills and manage the new technology they could not raise the $2,000 billion needed to build the world Smart Grid.

Our report suggests that a new business model for the development of Smart Grid in many countries, particularly the UK, could be based around capital investment coming from sovereign / state owned investment and pension funds; possibly from the Middle East and Asia. The day to day operation of balancing and operating Smart Grid would still be the responsibility of the utility companies whilst the IT and Communication companies would supply and operate IT infrastructures and the billing and pricing mechanism.

Strategic Acquisitions in the Smart Building to Smart Grid Space

…markets: smart grid, efficient infrastructures, and smart cities. The company is working on “smart city” projects in the U.S., France and China that link buildings and the grid. In May…

Smart Grid – The Renaissance of the World’s Electrical Transmission & Distribution Industry

…smart grid technology. In the meantime the world has confirmed the need to drastically reduce CO2 emissions and thus the need for a “Smart Grid” was born. Memoori has been…

Smart Grid – Report on Size, Structure & Growth

Any reader looking through the media content on smart grid for the first time could be forgiven for assuming that smart meters and the smart grid are one and the…

The Consumer Interface of the Smart Grid Business is where the Building Controls Suppliers are now Focused

…for Honeywell’s international services business. Lets be quite clear, the Smart Building to Smart Grid Interface Business is a relatively small business compared with Smart Grid. Our report http://memoori.com/smart-buildings-2012 estimates…

Building on the Edge: The Untapped Efficiency of Smart Grid Connection

…turn buildings into virtual power plants. The grid edge is the next step for buildings and the grid in our path to a smarter and more efficient world. “Grid edge is…

Smart Grid Suppliers Position for the Big Move into Automatic Demand Response

…first forays into the Smart Grid space. In September Cisco completed its acquisition of privately held Arch Rock Corporation, a pioneer in IP-based wireless network technology for Smart Grid applications….

Smart Buildings Can Be ‘The Nodes’ Of The Smart Grid

“As nodes of the smart grid, smart buildings will become increasingly active participants in the energy eco-system, moving beyond simply being served by the Smart Grid, they can also become…

Next Page