This Research Note examines what’s behind Identiv’s latest move to divest its physical security business to European security solutions player, Vitaprotech.

We review the new IoT business and the transaction details in the context of Identiv’s strategic review and 2023 financial performance, before exploring the implications for Vitaprotech.

This article is based on Identiv’s Strategic Review Presentation, 3rd April 2024, 2023 results and supplementary analysis of the Vitaprotech group.

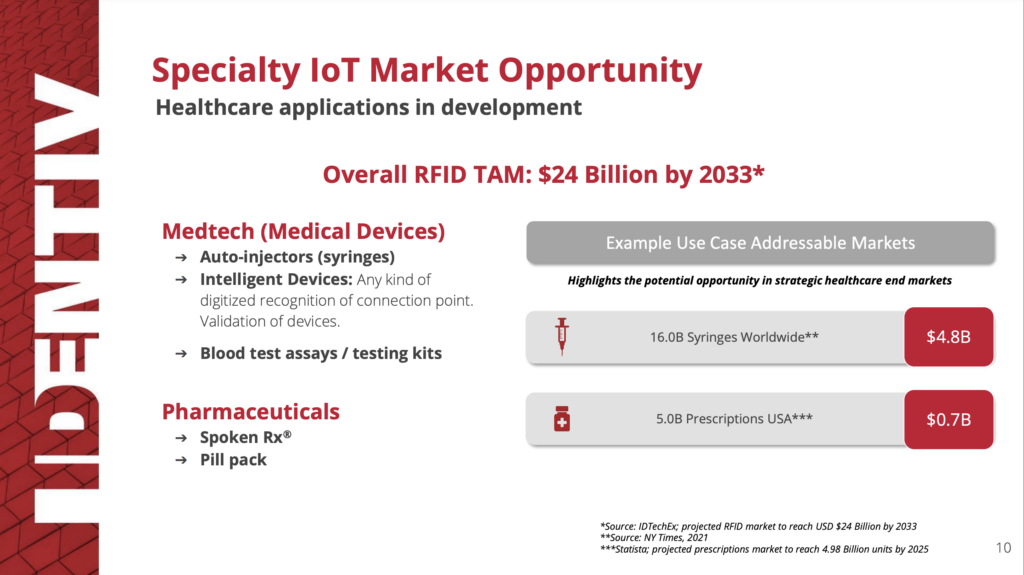

New Identiv IoT Business

Following a strategic review, Identiv has decided to divest its physical security business and focus on its IoT solutions business which is centred on RFID technology.

Identiv expects to realign their growth strategy with a particular focus on healthcare-related segments and other high value-add opportunities for which they believe their technology can be both differentiated and transformational.

As the healthcare industry and its providers advance their digital transformation, Identiv’s aim is to ensure that its technology and core competencies deliver a compelling value proposition for patients, physicians, providers, and payors, and address the critical unmet needs in healthcare around data science, compliance, utilization, effectiveness, and efficiency.

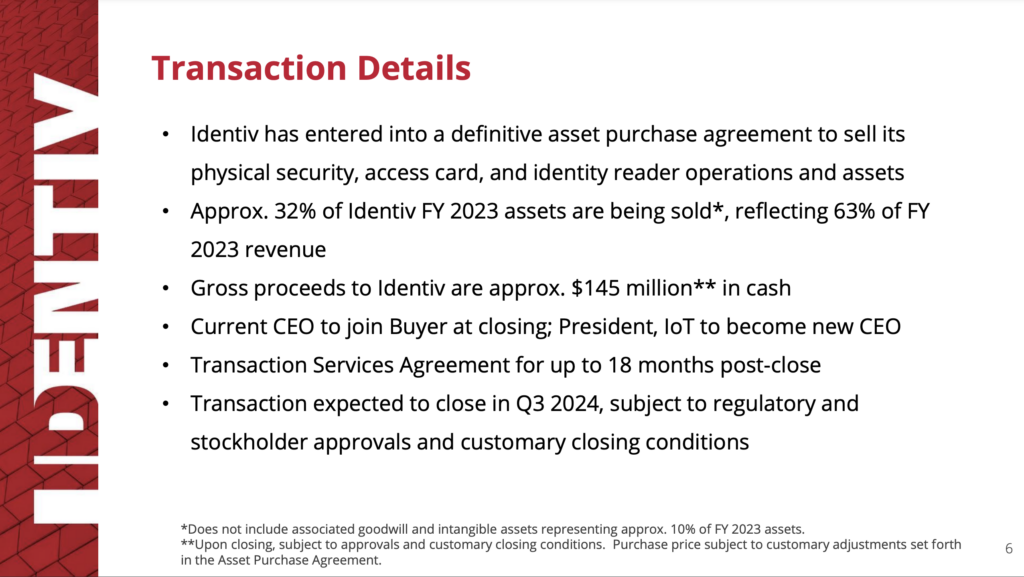

Transaction Details

On 3rd April 2024, Identiv, Inc. announced that it had entered into a definitive asset purchase agreement to sell its physical security, access card, and identity reader operations and assets to Vitaprotech, a French security solutions provider.

The proceeds from the sale will significantly strengthen Identiv’s financial position, generating capital to fund future organic and inorganic growth of its specialty IoT solutions business. Under the terms of the agreement, Identiv will receive a cash payment of $145 million upon closing of the transaction, which is expected in the third quarter of 2024.

Approximately 32% of Identiv FY2023 assets are being sold, reflecting 63% of FY 2023 revenues. With $73.3 million revenues divested, the transaction amounts to a sales exit multiple of 2.0.

Memoori expects that this relates to the entire Premises segment business, which amounted to $48.3 million revenues in 2023, and in addition a proportion of its Identity segment relating to identity readers operations and assets.

Key products in the Premises segment include the Hirsch and 3VR brands, Primis on-site access control hardware and software, Freedom encrypted access control, uTrust TS card readers, and Velocity Vision video management software.

Identiv Financial Highlights 2023

Revenue for fiscal year 2023 was $116.4 million, a 3% increase from $112.9 million in fiscal year 2022. By segment, Identity revenues were $68.1 million and Premises revenues were $48.3 million in fiscal year 2023.

GAAP net loss in fiscal year 2023 was ($5.5) million, or ($0.29) per basic and diluted share, compared to GAAP net loss of ($0.4) million, or ($0.07) per basic and diluted share, in fiscal year 2022.

Vitaprotech

Vitaprotech is the result of the 2014 merger of Sorhea, a specialist in perimeter intrusion detection for critical infrastructure and sensitive sites in France, and TIL Technologies, a French provider of access control software.

Headquartered in Vaulx-en-Velin, France, the Group currently comprises 14 companies, employing over 400 people in France, Germany, the UK and the US. Vitaprotech addresses customer needs through an integrated offering built around three complementary areas of expertise:

- Perimeter Intrusion Detection systems offered by Sorhea, Protech and Harper Chalice Group.

- Access Control & Management offered by ARD, TDSi, Vauban Systems and TIL Technologies.

- Intelligent Monitoring and Video Surveillance offered by Foxstream, Prysm Software, ESI, Videowave, RECAS and GS4.

We covered this group in our September 2022 Examined article. Since then, the Group has achieved revenues of more than €82 million in 2022 and reported more than €100 million in 2023. The combined group will generate revenues in excess of $185 million with more than 700 employees worldwide.

Vitaprotech’s goal to strengthen its presence in physical access security for critical and sensitive sites has certainly been achieved through the acquisition of Identiv’s North American physical security business, which is well known, particularly for high-end premium solutions in government agencies and commercial organizations.

Memoori View

Identiv's financial results have fallen short of market expectations over the past year, leading to a significant decline in its stock price. The company's struggles with revenue growth, widening losses, and concerns about its future profitability appear to be the primary reasons for its underperformance and its strategic decision to sell its physical security unit and focus on specialized IoT business.

This article was written by Daphne Tomlinson, Senior Research Associate at Memoori.