In this Research Note, we examine Skyfii, a Sydney-based Australian public company providing crowd analytics and occupancy management solutions to public venues and commercial properties. This analysis covers their latest financial results y/e 30 June 2023, investor presentations and their strategic review.

Skyfii completed an IPO on the Australian Stock Exchange in 2014. The company positions itself as a global omnidata intelligence company which is transforming the way organisations collect, analyse and extract value from data. They exist to help physical venues use data to better understand visitor behaviour and improve experience.

Skyfii ingests data from a diverse range of technologies including WiFi, cameras, people counters, LiDAR, and IoT devices. They combine these datasets with contextual data such as weather, retail sales and sociodemographic data to improve operational performance for retail properties, airports, stadiums, smart cities and other public and commercial venues.

Data analytics solutions are currently provided to over 12,000 venues in APAC, EMEA and the Americas region. Skyfii is intent on expanding its global footprint in the rapidly growing omnidata intelligence sector, in which the company processes more than 11 billion data points daily.

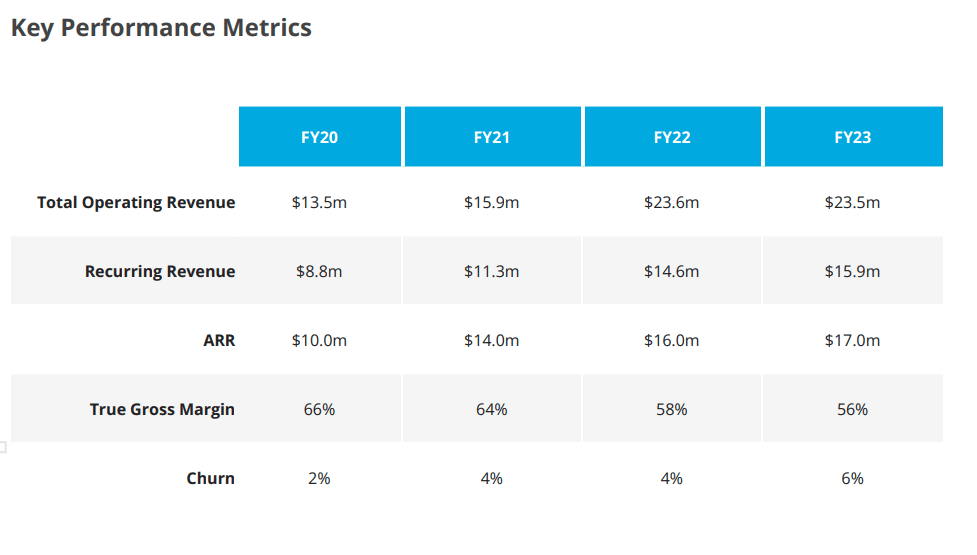

Skyfii FY2023 Highlights (in AUD$)

- Total operating revenues of $23.5m, down 0.4% vs FY2022

- Recurring revenue of $15.9m, +9% vs FY2022

- Delivered positive unaudited underlying EBITDA of $6k in 2H FY23 in line with guidance.

- Secured over $15.8m in new business Total Contract Value (TCV)

On 9th August 2023, the Skyfii Board announced the completion of a strategic review aimed at pursuing accelerated growth and resetting its operating cost base to achieve greater efficiency and generate improved and sustainable positive cash flows. Key decisions were as follows:

- Transition the leadership of Skyfii to a new CEO, with Wayne Arthur remaining available to the company over the next four months while a full-time CEO is identified.

- Focus on high-margin scalable vertical markets of retail & retail property, major transport hubs, sporting stadia & events and quick-service restaurants (QSR).

- Reduce headcount cost by 12% through improved efficiencies.

- Transfer of specific support and operations resources to newly established lower-cost operating hubs (Phillippines and Portugal).

- Retirement of non-core legacy products, with $0.6m in annualised recurring revenue at risk. The revenue associated with these products is low margin and will have a limited impact on profitability and cash flow.

Specific outlook for Skyfii throughout FY2024 include:

- Focus on core high-margin high-growth verticals, specifically airports, stadiums, retail and quick-service restaurants.

- Conversion of over $33m pipeline in qualified stage deals.

- Operating cost savings through delivery of transformation initiatives.

This article was written by Daphne Tomlinson, Senior Research Associate at Memoori.