This article was written by Daphne Tomlinson, Senior Research Associate at Memoori.

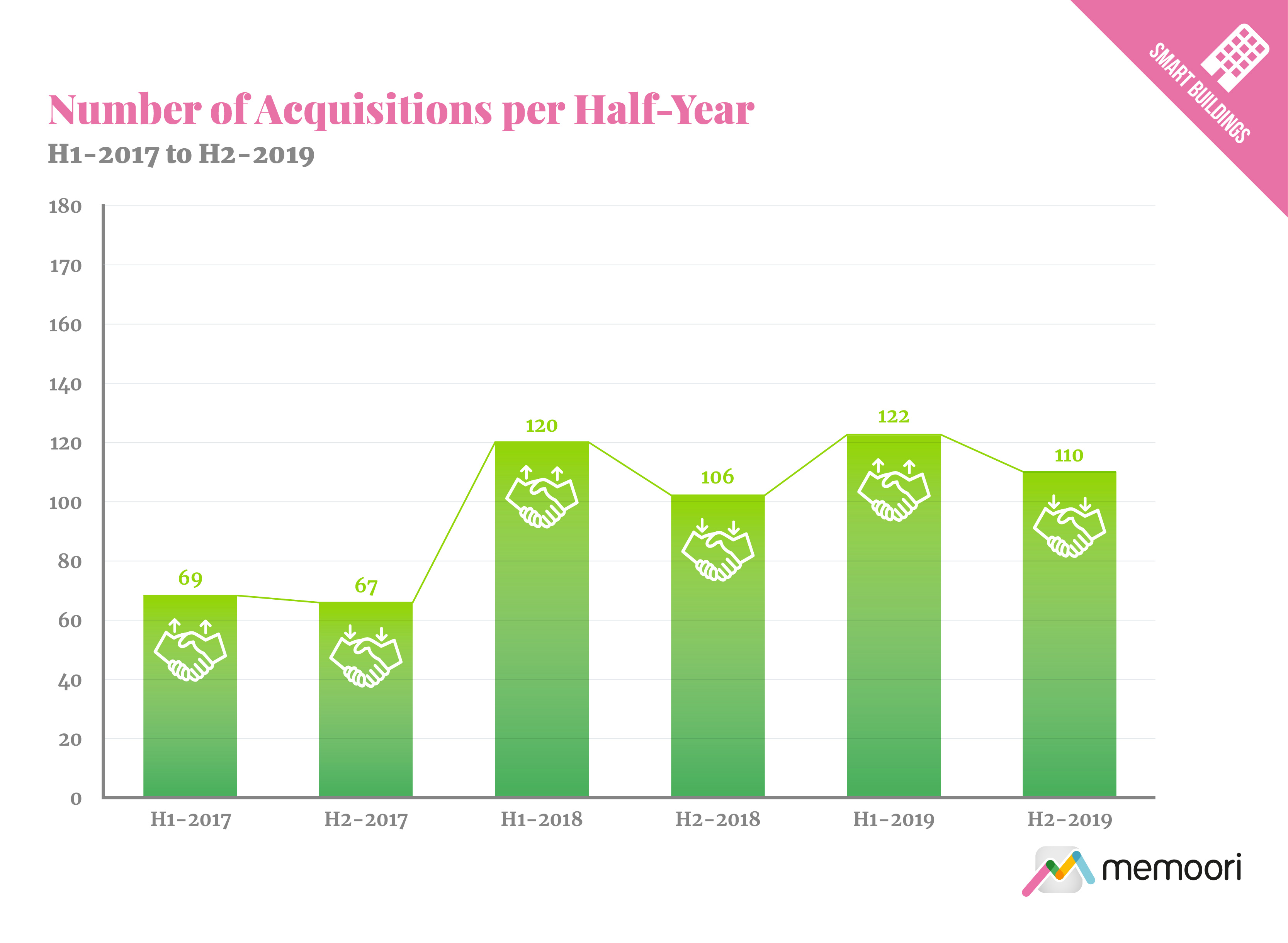

Over the last three years, Memoori has tracked 594 acquisitions across the smart buildings space, described in detail in our new report on M&A and Investments in Smart Buildings H2-2019.

Record levels of M&A in the last 2 years are confirming a shift in the slowly evolving market, with 232 acquisitions in 2019 and 226 in 2018, which was a 66% increase over 136 in 2017. This heightened level of activity maintained over the last 2 years is a significant indicator that a tipping point has finally been reached in the acceptance and adoption of intelligent building technology.

In the building automation and proptech segments, we saw considerable activity in the acquisition of IoT technology to enhance the workplace experience of building occupants and to sense, control, visualize, monitor and predict a range of operational parameters to improve building performance. 202 acquisitions in these segments were tracked by Memoori in the last two years since Jan 2018, of which almost 60% were technology startup companies who achieved exits through acquisition.

Recognizing they cannot necessarily deliver leading solutions for all building segments, established players are buying startup technologies as a low-risk solution to keep up with the pace of digital innovation. With the support of their new owners, these companies are gaining a foothold in the emerging markets for AI-based IoT platforms for buildings, workplace management, occupancy analytics, in-building location systems, connected lighting, digital locking, video analytics and more.

The physical security and safety segment was dominated by an accelerated pace of M&A as regional integrator firms were acquired by larger national companies, backed by private equity finance. Even so, the commercial security market remains highly fragmented.

Software was the predominant theme for acquisitions in building energy management, and the building to grid category. Acquisitions in the Smart Home segment were comparatively small in number (51 in the last two years) but there were some high value transactions in this period, (eg. Vivint Smart Home, Control4, Ring, SimpliSafe)

One significant trend is the diversity in the range of buyers entering the smart buildings space. We have seen acquisitions by stakeholders from across the building lifecycle, including real estate service firms, engineering consultancies, energy service and utility companies, software providers, building systems vendors, facilities management service firms and ICT companies.

We expect this high level of M&A activity to continue across the global commercial smart buildings market into 2020, as some technologies prove to be winning assets, other solutions are sold to more appropriate owners, platforms consolidate and major players rationalize their portfolios.

Memoori’s latest report on M&A and Investments in Smart Buildings H2-2019

consists of 70 slides and supporting spreadsheets with complete listings of acquisitions and

investments covering 3 years since January 2017, based on Memoori’s database of deals. The report includes 20 company profiles of acquisitions and investments together with 20 profiles of buyers and investment firms, presenting our view of their respective strategies and significant M&A or investment activity. Key technology segments in the report are covered in 7 categories:

- 1. Building Automation includes building controls, building management systems, Internet of Things in buildings, platforms and software, enablement hardware, sensors, networking and connectivity, cyber security, connected lighting, connected HVAC and systems integration.

- 2. Proptech includes workplace management platforms, IWMS, tenant experience software, occupancy analytics and space utilization, indoor mapping and location services, building asset and maintenance management solutions, indoor air quality and technical facilities management.

- 3. Physical Security & Safety includes access control systems, intruder detection, perimeter protection, video surveillance, video analytics, identity management, biometrics, PSIM, digital locking, emergency response, critical infrastructure protection, mass notification systems, fire detection and systems integration.

- 4. Building to Grid includes smart metering, meter data analytics, demand response platforms, distributed energy storage and resource management, microgrids and virtual power plants.

- 5. Building Fabric includes smart glass and windows, solar photovoltaics, green roofing and walls and smart flooring.

- 6. Building Energy Management includes energy efficiency and analytics software, sustainability platforms and energy services.

- 7. Smart Home includes building technologies from all preceding six segments focused on application in residential properties including home energy management, security systems, smart thermostats and water management.

Follow to get the Latest News & Analysis about Smart Buildings in your Inbox!