Memoori have been collecting and analysing global M&A data in the Physical Security Industry covering the last 18 years. This article looks at the trends that have taken place over this period driven by the need for consolidation built around innovative products that deliver solutions. We review the impact M&A has had on developing winners and compare against equally successful companies that have grown solely through organic growth.

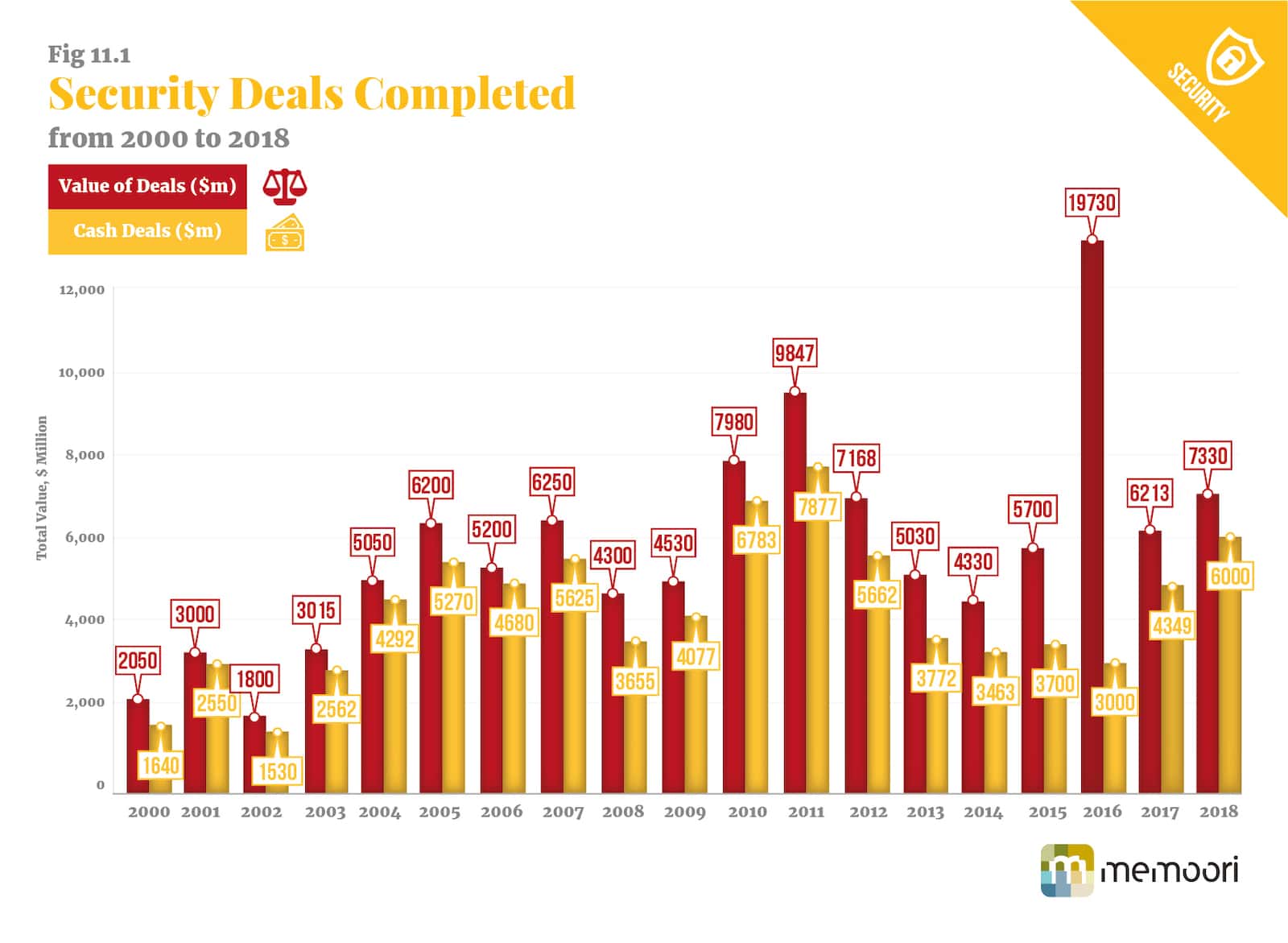

Over the last 18 years the Physical Security industry, has gone through four cycles of rise and fall in the value of activity, sometimes exaggerated by a number of billion dollar deals in one year, such as the merger of Johnson Controls and Tyco of $16.5Bn in 2016. The total value of deals in 2016 was $19.73 billion making it almost three and a half times larger than the previous year. Nevertheless as the chart below shows over this period there is a general upward trend in consolidation of the industry, which has grown by a CAGR of 7.5% from 2000 to 2018.

In 2018 mergers and acquisitions at $7.33Bn, looks like the start of a new wave of growth. The structure of the industry is still very fragmented with hundreds of small companies finding it increasingly difficult to compete in this price competitive market and it looks inevitable that the general trend line of value and volume of M&A will continue upwards over the next 5 years but at a slightly lower rate of growth.

We would have expected the need to scale up growth through strategic acquisition particularly for western manufacturers would have been paramount but it has not happened this year. There is a paucity of companies over $400m revenue in the video surveillance industry that would be possible targets for acquisition that could rapidly build up scale and help alleviate the problem of the “race to the bottom”.

HIKvision and Dahua now take well over 40% of the world market for video cameras; and did this by adopting a strategy of reducing prices and rapidly building up volume. They have been able to do this through organic growth based on their protected and very large home market. Even given that their growth has recently declined, provided their home market stays buoyant they look like increasing (at a more modest growth rate) their share even more. Neither company has acquired businesses of any size and have built up their business through organic growth; So far they have not resorted to strategic acquisitions of any real size.

Follow to get the Latest News & Analysis about Smart Buildings in your Inbox!

Another significant trend which changed the structure of the market for Fire and Security solutions is that during the period 2000 to 2010, conglomerates such as GE, Honeywell, Schneider, Siemens, UTC, and Tyco were firmly amongst the world's leading suppliers. Since then the performance of conglomerates has declined particularly in the physical security business and some have sold off these businesses.

The conglomerates mainly built up through acquisition are for the most part no longer interested in the physical security products business, but will continue to operate in the systems business. They have failed to develop a profitable business because the specialist security manufacturers have developed better performing products at more competitive prices. At the same time the conglomerates have competed with the independent SI’s in the systems business which has had a detrimental impact on their product business.

In the video surveillance business we have identified a number of very successful acquisitions with two cross boarder acquisitions that stand out. Canon acquired Axis Communications the leader in IP Cameras and Milestone the leader in Video Management Systems in 2015 and 2014 respectively. They have operated successfully for four years now with the same management team and little interference but financial backing when needed.

In the Access Control business HID Global have completed multiple acquisitions over the last 10 years that have made a major contribution to their profitable growth and similarly Vanderbilt have built up a successful company through strategic acquisitions. Our new research report shows that in the last 10 years we have identified 742 deals and these examples represent a small proportion of all successful acquisitions.

The value and volume of acquisitions has increased over the last 4 years even when we adjust for the distortion caused by bumper M&A deals such as the Johnson / Tyco deal in 2016 and Thales / Gemato in 2018. The number of deals in the range of $50m to $150 has increased and there has been more diversity across the different product types.

In 2018 deals over $100m that we believe will have a significant impact on the Physical Security business include;

Avigilon has finally been acquired but not by a competitor but by Motorola Solutions for $1bn which was not an expensive buy. It would seem that Motorola is aiming to increase activity in the wider public safety and ‘safe city’ market. They offer total systems business and Avigilon are a products manufacturer and this may cause conflict of interest with Avigilon’s customers. This acquisition will bring Avigilon's advanced video surveillance and analytics platform into public safety, while expanding their portfolio of new products and technologies for commercial customers.

The Thales / Gemalto acquisition of $5.5Bn paid in cash creates a powerhouse with a solution portfolio including security software, expertise in biometrics / multifactor authentication and the issuance of secure digital and physical credentials. Gemalto’s offerings also include digital security for enterprise and the cloud (which spills over into the Internet of Things) along with EMV chip cards, NFC for mobile phones, SIM cards and authentication for online banking.

UTC Climate, Controls & Security reached an agreement to acquire S2 Security, a leading developer of unified security and video management solutions. No financial details were given but it is estimated to have cost at least $200 million. This move is well aligned with their strategic focus to grow their core business. The company provides enterprise physical security solutions, including access control, video surveillance, event monitoring, digital signage, live Internet sourced real-time data and information feeds, mobile applications and cloud-based services.

HID Global a seasoned practitioner of acquisitions acquired Crossmatch a leader in biometric identity management and secure authentication solutions, from private equity firm Francisco Partners. HID together with its parent Assa Abloy are the most acquisitive companies in the Physical Security Industry.

For more information on M&A and Investment in the Physical Security market, read our report - The Physical Security Business 2018 to 2023.