New Research from Memoori http://memoori.com/portfolio/thephysicalsecuritybusinessin2013/ demonstrates that the geographic distribution of sales of security products is clearly changing with Asia becoming the dominant region.

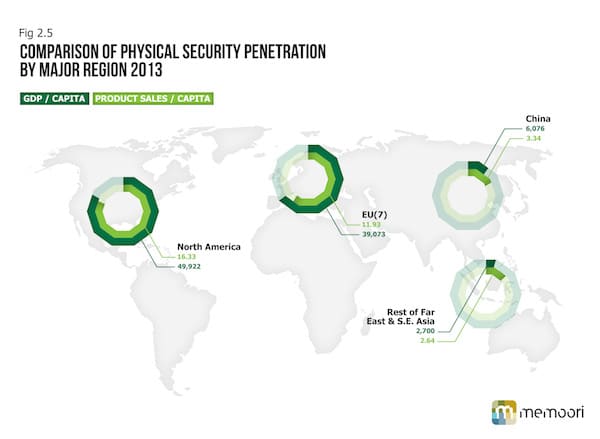

A major change in the geographic distribution of sales is taking place with Asia delivering the highest rate of growth and increasing its market share. This is set to continue because there is still a massive latent demand waiting to be exploited. In China penetration is almost an order of magnitude smaller than North America and well before this has been mined the Chinese market will be larger than the US.

In the rest of Asia (including India) the penetration chart shows that this area has a lower level of penetration than China. There are a number of countries in this group that have large populations such as India, Indonesia, The Philippines and Vietnam. These countries have dragged down the penetration to $1.9 per capita. However Japan, Australia, South Korea and Singapore have much higher penetration of security on a parallel to western countries.

Asia in general and China particularly are markets that western companies need to take a long-term approach to, because they are difficult markets to penetrate. Despite a fall in GDP growth in the last few years demand for physical security in China has forged ahead delivering a CAGR of some 25 to 30% over the last 5 years, the highest growth recorded in our industry and there is no indication that growth will fall off in the near future.

One of the reasons for this is that the penetration of security systems in China is still remarkably low and the more expensive IP Networking products only account for a small proportion of sales. The GDP per capita in 2012 is projected at $6,120, and sales per capita was $3.34 per capita showing that the potential for future growth is enormous and could grow 6 times to equal the current penetration level in North America.

Why is it that US and European manufacturers are not making a better job of exploiting the Chinese market? Conversely why is it that Chinese manufacturers are having difficulty in establishing a solid presence in the developed markets of the world with the exception of delivering through OEM (Own Equipment Manufacturers) channels.

Could these 2 problems be solved by M&A and alliance between the new breed of public companies in China and the leading edge companies of the West? Both have strengths to offer that compensate each other’s weaknesses and therefore together they are stronger than the sum of their parts.

To achieve such a union requires complete trust but unfortunately in the past some companies have shown little regard for respecting patents and protected technology. However recently Ubiquity has won a case in China to stop the pirating of its technology so a precedent has now been set that patents and technology can be protected.

Whilst China is mostly dominated by indigenous manufacturers, it does not yet have a company that strides the international stage comfortably with products right on the bleeding edge. Hikvision come closest and in August last year a rumor surfaced that it was in talks with Schneider Electric (Pelco) to discuss how they could work together. Nothing was officially announced but the rumor returned in February.

China is developing a strong indigenous manufacturing supply industry and in particular 2 companies Hikvision and Dahua are growing fast increasing their share of the local market. They have also been taking product business away from Taiwanese and Korean manufacturers in western markets.

Hikvision sales in 2012 were somewhere around $1.2 billion, a growth of 40% over 2011 and of this export product sales of DVR/ camera equipment was around 35%. Hikvision’s latest Q1~Q3 report showed total assets around US$2b. At per share value of about RMB$32 and about 2 billion shares available (2,008,611,611 at the end of Sept 2012) giving it a valuation of US$10 billion.

The majority of growth has come from domestic acquisitions, of access control, guarding services and specialist vertical market systems integration companies. They are developing a similar model to Honeywell and Schneider Electric of developing a systems and product business separately.

Some 15 years ago fire detection systems in China moved almost overnight to analogue addressable systems that cost double the price of conventional technology and no local manufactures could supply them. Imported products flooded in and the local system installers quickly learn how to install them. Although moving from analogue to IP requires more skill, it will happen, and in China it will come quickly.

Price is no longer king in western markets but cost of ownership made up of many factors is; and this will also apply in China as IP takes hold and offers many different and improved solutions.

Whilst M&A may not be a serious proposition at this time, alliance is the precursor of acquisition. Combining Western IP technology for the Chinese market pushed through indigenous manufacturers channels of distribution and Chinese products into the western markets through an alliance partner channel of distribution could bring benefits to all parties.

Memoori’s report “The Physical Security Business in 2013” is a definitive resource for Security Market Research & Investment Analysis. For more details, please visit - http://memoori.com/portfolio/the-physical-security-business-in-2013/