The vision of smart buildings, as presented by the media and marketing departments, depicts a technological utopia with broad sensory capabilities, intuitive human-centric applications, and advanced intelligence. This vision might be technically possible, but currently even the path to a "semi smart building" is fraught with challenges that make technical development difficult. Challenges which are limiting adoption relative to smart buildings huge potential market and could even see current innovations become obsolete before reaching critical mass. We must stop looking at the smart building as the final destination, and begin to see it as the journey.

“The technical IoT solutions, in terms of hardware, connectivity, and software applications are broadly market ready and suitable for deployment for a variety of use cases, with increasing numbers of case studies demonstrating creditable returns and solution viability in a large variety of building types,” reads our latest market research on the IoT in buildings. “However, IoT solutions are getting inevitably more complex and dynamic. They involve larger ecosystems of devices and evolve quickly which means that achieving the highest levels of IoT functionality will remain a moving target for end-users.”

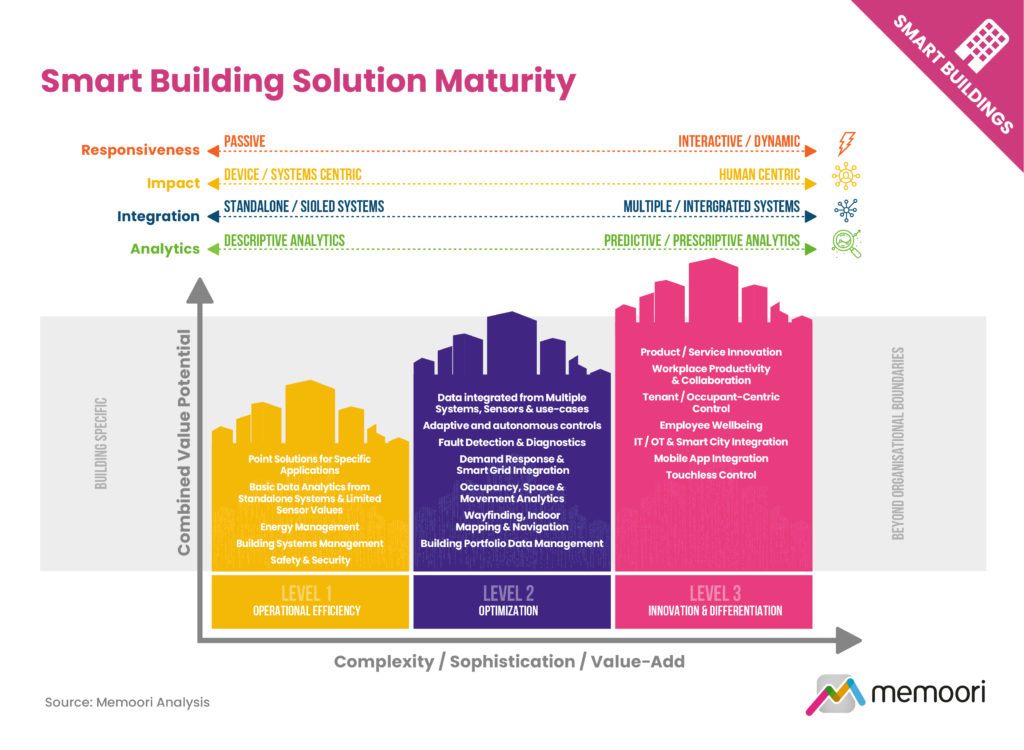

Consequently there is a huge variation in the level of sophistication of smart building initiatives amongst building owners and developers. To illustrate the varying levels of sophistication and value that can be achieved through IoT solutions in commercial smart buildings, Memoori has developed a model to ascribe three potential levels of smart building data solution maturity. The majority of commercial buildings currently lie at the beginning of the scale, with much of their installed equipment still not IoT enabled, and systems that remain largely incapable of effective digital communication and control.

For buildings to progress to level two in the model requires a much greater degree of integration between building systems, and can be facilitated by the adoption of open-protocols to enable systems interoperability. By integrating data from typically siloed data sources, building owners and operators can develop compound applications that incorporate data from multiple systems or devices. This allows for the development of autonomous solutions that can respond dynamically to events or changing conditions in or around the building, following sensor-based analytics data.

“Integrating real-time smart energy meters inputs with air quality sensors and occupancy sensor data that monitors building, floor or even desk level utilization, can empower analytics that highlight correlations between energy consumption and space utilization, for example. These analytics can then be used as dynamic inputs to HVAC and lighting systems that optimize energy and sustainability performance whilst still maintaining a comfortable in-building environment for building occupants,” reads the extensive study. “Where the BIoT has been deployed across the whole of an organization’s portfolio of buildings, operators and facilities managers gain the ability to gather and compare metrics across multiple facilities. This enterprise-wide view can be a valuable business intelligence asset.”

Attaining the third level of smart building maturity involves incorporating data from beyond the building itself to consider people, cities or even wider business objectives. By incorporating human inputs into an IoT system, building owners and operators can develop more holistic smart solutions. Level 3 innovations provide insights into behaviors, preferences and attitudes that help the organization to proactively engage with building users, delivering personalized solutions that help an organization develop meaningful relationships, trust, loyalty and satisfaction with building users. Successful delivery of level 3 solutions improves the overall attractiveness of the building due to its greater capacity to meet the demands of users - leading to increased lease value, higher occupancy rates, and higher sale values.

“The transition to level 3 in our model does not have to occur all at once, indeed attempts to jump straight to level 3 will likely end in a costly failure. A solid grasp of the systems and data analytics requirements of the kinds of systems deployed in Level 1 of our classification is also typically required to move up the value chain to levels 2 and 3 of the model,” reads the new report. “Aspiring to attain level 3 in the model from a standing start, end users are highly likely to experience unforeseen issues related to system interoperability, solutions not working as expected leading to poor data quality, as well as face challenges associated with delivering outcomes that effectively address the need and desires of the huge range of stakeholders involved.”

By treating smart building development as a journey, rather than a destination, building owners and managers can feel the achievement and progress of levels 1 and 2. As such, buildings should gradually phase in smart technology through a series of tangible, prioritized benefits that best service the needs of the business and its various stakeholders. Such an approach also helps to build trust and add value over time and can help owners and operators to develop the relevant skills and expertise over time, increasing efficiency and steadily reducing operational costs as they go. For most buildings, this phased development journey is the only way to achieve smart technology maturity and long-term building objectives.